Vlad Kalashnikov is Head of Products at CFOUR Comply, an inline XBRL (iXBRL) conversion software. Through direct involvement in customer onboarding, he works closely with teams navigating these requirements, giving him firsthand insight into the operational realities firms face with tagging and the challenges corporate service providers encounter delivering these services at scale.

Vlad Kalashnikov is Head of Products at CFOUR Comply, an inline XBRL (iXBRL) conversion software. Through direct involvement in customer onboarding, he works closely with teams navigating these requirements, giving him firsthand insight into the operational realities firms face with tagging and the challenges corporate service providers encounter delivering these services at scale.

The CSRD timeline has changed significantly since the directive was first adopted. Under the Omnibus I simplification package (Directive (EU) 2026/470, in force March 2026), mandatory CSRD reporting now applies to companies with more than 1,000 employees and more than €450m in turnover — a substantial reduction from the original scope. Wave 1 companies (those already reporting under the NFRD from 2024 data) are permitted to skip filings for 2025 and 2026 under a transition exemption. The next mandatory wave falls in 2028, covering 2027 fiscal year data. Non-EU companies are in scope if EU-group turnover exceeds €450m and the EU branch’s turnover exceeds €200m. This article outlines the full CSRD implementation timeline, the current thresholds, and the preparation steps organisations should be taking now.

This article covers the CSRD implementation timeline in detail. For a full explanation of what CSRD is and which companies it affects, see our overview of the Corporate Sustainability Reporting Directive: What is CSRD?.

The CSRD timeline is a priority for companies operating within the European Union. The Corporate Sustainability Reporting Directive (CSRD) introduces phased reporting requirements, expanding corporate sustainability disclosures.

This article outlines the CSRD implementation timeline, clarifies reporting phases and thresholds, and explains what steps your organisation can take to prepare. It also covers the updates introduced by the Omnibus I simplification package (Directive (EU) 2026/470, published 26 February 2026), which made significant revisions to CSRD scope and deadlines.

Understanding CSRD Reporting and Its Goals

What Is the CSRD?

The CSRD, enacted by the European Union, was created to improve corporate transparency in sustainability reporting. It builds on the Non-Financial Reporting Directive (NFRD), expanding the scope and introducing standardised reporting requirements.

Detailed Reporting. The CSRD requires detailed disclosures of sustainability-related information in the organisation’s management report.

Mandatory Assurance. Mandatory third-party assurance is required for sustainability disclosures. Under Omnibus I, the level of assurance is now limited assurance only (not reasonable assurance as originally proposed). The level of assurance was simplified under Omnibus I from reasonable assurance to limited assurance.

Digital Tagging. Sustainability information must be tagged in the management report and submitted in XBRL/iXBRL format.

CSRD Goals

Regulatory Compliance. Failure to comply with CSRD reporting requirements can lead to penalties and reputational damage, as well as reduced access to investment. Early preparation reduces these risks.

Stakeholder and Investor Expectations. Investors increasingly assess sustainable and responsible business practices. Transparent ESG reporting supports stakeholder confidence and investor access.

Alignment with EU Sustainability Goals. By complying with CSRD, businesses contribute to the EU’s broader climate and social objectives.

The CSRD Timeline: Who Reports and When?

The CSRD requires sustainability reporting from a defined set of entities, both within and outside the EU. Omnibus I (March 2026) significantly reduced the number of in-scope companies. Here is the current timeline by company group.

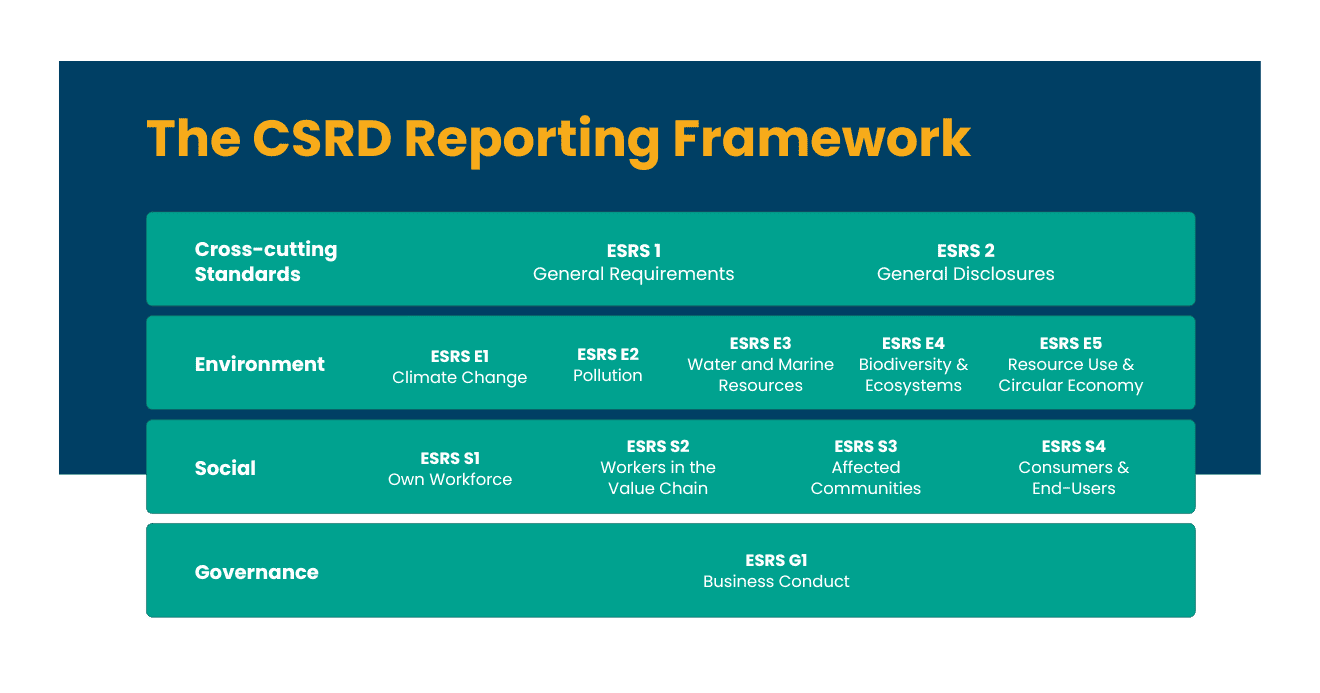

The CSRD Reporting Framework

The CSRD mandates reporting on Environmental, Social, and Governance (ESG) factors, aligned with the European Sustainability Reporting Standards (ESRS).

Since the Omnibus I simplification, the depth of assurance required for CSRD reporting has been eased in two key ways. First, sector-specific data requirements have been reduced, meaning companies no longer need to provide as granular sustainability information based on their industry. Second, supply chain data collection now focuses on direct suppliers only, rather than the full value chain.

Reduction of Sector-Specific Data

Omnibus I removes many of the sector-specific ESG reporting requirements that previously applied to industries such as energy, agriculture, and manufacturing. The reporting framework now operates on a more generalised basis for most sectors.

Narrowing Supply Chain Data Requirements

Omnibus I narrows the supply chain data requirement to direct partners only, unless significant risks are identified further along the chain. This removes the obligation to gather ESG data from the extended value chain.

Key Revisions of CSRD Under Omnibus I

Omnibus I (Directive (EU) 2026/470, published 26 February 2026, in force 18 March 2026) introduced the following revisions to CSRD:

- Scope reduction. Companies with fewer than 1,000 employees are now excluded from mandatory CSRD reporting. Only companies with more than 1,000 employees and more than €450m in turnover are required to report. This removes listed SMEs and large companies with fewer than 1,000 employees.

- Wave 1 transition exemption. Companies in Wave 1 (NFRD reporters filing from 2024 data) may skip CSRD filings for 2025 and 2026 under the transition provisions. Omnibus I transition exemption for Wave 1.

- Extended deadlines. The Wave 2 reporting deadline has moved from 2026 to 2028, with reports based on 2027 fiscal year data. Listed SMEs that were originally scheduled for 2027 are no longer in scope. Non-EU company deadlines remain at 2029 for 2028 fiscal data.

- Simplified reporting framework. Sector-specific ESG standards have been removed.

- Narrower supply chain reporting. Companies now collect sustainability data from direct partners only.

- Limited assurance only. The earlier requirement for reasonable assurance has been replaced with limited assurance for sustainability disclosures.

For a detailed review of the specific regulatory changes, see our breakdown of the CSRD rule changes under Omnibus I.

Preparing for CSRD Compliance

The scope and detail of CSRD reporting require structured preparation. Companies currently in scope (more than 1,000 employees and more than €450m turnover) should work through the following steps:

- Confirm your submission period. Identify which reporting wave applies to your organisation and the relevant fiscal year.

- Conduct a double materiality assessment. Evaluate both the impact of your operations on the environment and society, and how sustainability factors affect your company’s financial performance. Guidance is available from EFRAG, including EFRAG IG 1: Materiality Assessment and EFRAG IG 2: Value Chain. Under Omnibus I, these guides are being revised to reflect the reduced supply chain scope.

- Prepare a data gap analysis. Identify which ESRS data points are material to your organisation and whether existing data collection processes cover them. Reference EFRAG IG 3: Detailed ESRS Datapoints and the accompanying Explanatory Note.

- Collect required data on material topics. Establish processes for consistent data collection across all required indicators.

- Structure your report according to ESRS requirements. ESRS 1 provides the required structure, covering General Information, Environmental Information, Social Information, and Governance Information.

- Select an appropriate tool for CSRD digital tagging. Modern reporting platforms, such as CFOUR Comply for CSRD reporting, support XBRL/iXBRL tagging of sustainability reports.

The Case for Early Preparation

For finance and sustainability leaders, CSRD compliance carries implications beyond regulatory adherence. Transparent ESG reporting supports investor confidence and aligns with the EU’s long-term sustainability policy direction.

Delaying preparation increases risk: late-stage data gaps, internal coordination failures, and rushed digital tagging create more errors and higher remediation costs. Identifying your tool early and testing the tagging process on draft reports is the most effective way to reduce submission-period pressure.

To see how CFOUR Comply handles CSRD digital tagging, request a demo.

The CSRD Timeline and Reporting - Frequently Asked Questions

- What is the CSRD implementation timeline?

The CSRD timeline has been revised by Omnibus I (in force March 2026). Wave 1 companies (NFRD reporters) submitted their first CSRD reports in 2025 covering 2024 data but may skip 2025–2026 filings under a transition exemption. The next mandatory wave falls in 2028, covering 2027 fiscal data, for large companies with more than 1,000 employees and more than €450m in turnover. Non-EU companies must report from 2029 for 2028 data if the relevant EU-group thresholds are met.

- When did CSRD reporting start?

The CSRD came into force on 5 January 2023. Wave 1 reporting (for 2024 fiscal data) began in 2025, covering companies previously subject to the NFRD. Omnibus I (March 2026) introduced a transition exemption allowing Wave 1 companies to skip 2025 and 2026 filings.

- Who was required to report in 2025?

Wave 1 in 2025 covered companies previously reporting under the NFRD. These include companies with over 500 employees, net turnover exceeding €50m, and assets above €25m. Omnibus I introduced a transition exemption allowing these companies to skip filings in 2025 and 2026.

- What happens if a company misses CSRD deadlines?

Non-compliance can result in financial penalties and reputational harm. Investors, customers, and other stakeholders assess ESG disclosure quality, and a gap in reporting can affect access to capital and commercial relationships.

- Are SMEs required to report under CSRD?

Under Omnibus I, listed SMEs are excluded from mandatory CSRD reporting. They may choose to report voluntarily under the VSME standard based on EFRAG’s framework. Mandatory SME reporting may be introduced in future regulatory cycles.

- What did the Omnibus I simplification change about CSRD?

Omnibus I (Directive (EU) 2026/470, in force March 2026) made six significant changes. It narrowed scope to companies with more than 1,000 employees and more than €450m turnover; introduced a Wave 1 transition exemption for 2025–2026; postponed the Wave 2 deadline from 2026 to 2028; removed sector-specific ESG standards; narrowed supply chain data requirements to direct partners only; and replaced reasonable assurance with limited assurance.